High Credit Card Debt Impact on Net Worth – Reduce Debt, Increase Wealth

Anam Banu Chhipa

December 10, 2024. 4 minute Read

Imagine this: You’re earning well, but every month, a significant chunk of your income disappears into paying off credit card bills. It’s a common scenario, and it can be stressful and overwhelming. High credit card debt can be like a silent thief, slowly eroding your net worth and jeopardizing your financial goals.

But you’re not alone!

In India, credit card debt is rising rapidly, and many individuals are grappling with its implications.

"

In this article, we will explore how high credit card debt impacts your net worth, why it hinders your financial aspirations, and most importantly, practical strategies to reduce debt and increase wealth.

How Does High Credit Card Debt Impact My Net Worth?

Net worth is a simple equation:

Net Worth=Total Assets – Total Liabilities |

Think of it as your financial scoreboard. Assets are what you own, like savings, investments, and property. Liabilities are what you owe, including credit card debt, loans, and mortgages.

Credit card debt is a liability that directly impacts your net worth. When you carry a high balance on your credit cards, it increases your liabilities, dragging down your net worth. High credit card debt can even lead to a negative net worth, meaning you owe more than you own.

For Example:

- Let’s say your assets (savings, investments, property) are worth ₹15 lakhs.

- You have a credit card debt of ₹5 lakhs.

- Your net worth is ₹10 lakhs (₹15 lakhs – ₹5 lakhs).

If your credit card debt increases to ₹7 lakhs due to overspending, your net worth drops to ₹8 lakhs.

The Vicious Cycle of Interest

Credit cards are notorious for their high interest rates, often exceeding 30% annually. If you only make the minimum payment on your credit card debt, you’ll end up paying a huge amount in interest over time. This can trap you in a cycle of debt, making it seem almost impossible to catch up.

For Example:Imagine you owe ₹50,000 on a credit card with a 20% interest rate.

If you only make minimum payments, it could take years to clear the debt, and you’ll end up paying thousands of rupees in interest. This interest is money that could have been used for savings or investments.

How Credit Card Debt Sabotages Financial Goals?

High credit card debt doesn’t just affect your present net worth, it can also derail your future financial goals!

Here's how:

- Stifles Savings and Investments: High credit card debt eats into your disposable income, leaving less to save or invest. Delaying investments means missing out on the power of compounding, which can significantly impact your long-term wealth.

- Fuels Financial Stress: The constant worry of credit card debt can lead to anxiety and stress, affecting your mental and physical well-being, relationships, and work performance. Studies show that financial stress is a major contributor to health problems and can create a cycle that's hard to break.

- Limits Opportunities: High credit card debt can impact your credit score, making it harder to get loans for a home, car, or education at favorable rates.

For Examples:

Ajay, a young professional, delayed investing in mutual funds because of a ₹1 lakh credit card debt. He realized that the delay cost him ₹5 lakhs in potential returns over five years.

A study found that individuals who carried high levels of unsecured debt, like credit card debt, were 76% more likely to experience pain that interfered with their daily lives, compared to those with no unsecured debt.

Strategies to Reduce Credit Card Debt and Increase Net Worth

It’s time to take control! Here are some actionable strategies to help you reduce your credit card debt and boost your net worth.

1. Master the Art of Budgeting

The first step to tackling any financial problem is understanding where your money is going. Trackyour income and expenses to identify areas where you can cut back and allocate more towards debt repayment.

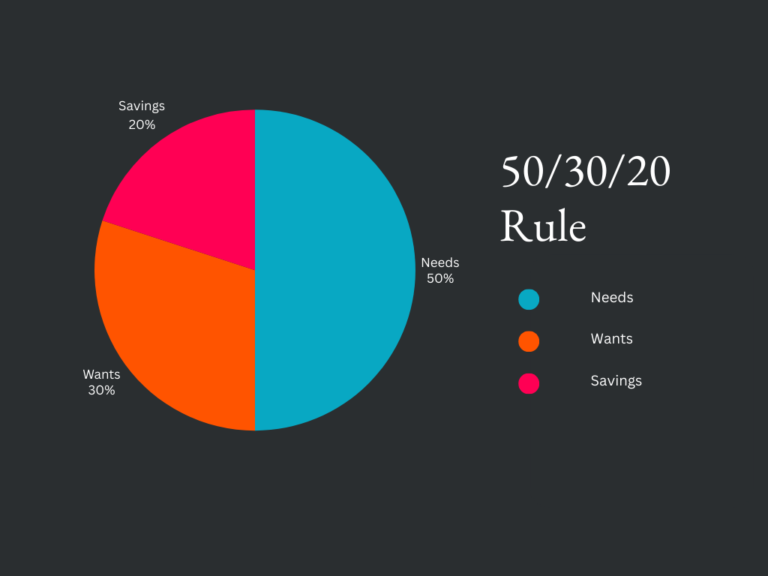

- Use the 50/30/20 rule: Allocate 50% of your income for needs (essentials like rent, groceries, utilities), 30% for wants (non-essentials like entertainment and dining out), and 20% for savings and debt repayment.

- Budgeting apps like Walnut, YNAB, or Money View can help you stay organized and track your progress.

2. Strategize Your Debt Repayment

Use these following methods below to strategize your debt repayment.

- Snowball Method: Pay off the smallest debts first to gain momentum and motivation. As you pay off each debt, you'll feel a sense of accomplishment and be encouraged to tackle the next one.

- Avalanche Method: Pay off the highest-interest debts first to minimize the total interest you pay over time. This method saves you money in the long run.

3. Explore Consolidation and Negotiation

- Debt Consolidation: If you have multiple credit cards with high balances, consider consolidating them into a single loan with a lower interest rate. This can simplify your payments and save you money on interest charges.

- Negotiation: Contact your credit card issuer and negotiate for a lower interest rate or more favorable repayment terms. You might be surprised at how willing they are to work with you, especially if you have a good payment history.

For Example: Rahul, an engineer, negotiated a 12% EMI plan for his ₹80,000 credit card debt, saving ₹10,000 in annual interest.

4. Build Your Emergency Fund

Having an emergency fund of 3-6 months of living expenses can protect you from falling back into credit card debt when unexpected expenses arise. Start small and make consistent contributions to your emergency fund every month.

5. Seek Expert Advice

If you’re struggling to manage your debt, don’t hesitate to seek professional guidance from a financial advisor or enroll in debt management programs. They can provide personalized advice and create a tailored debt management plan to help you achieve financial stability.

6. Invest in Financial Literacy

- Understanding the basics of interest rates, credit scores, and budgeting can empower you to make informed financial decisions.

- Explore free financial literacy programs offered by institutions like the Reserve Bank of India (RBI) and the Securities and Exchange Board of India (SEBI).

Final Thoughts

In Conclusion!

High credit card debt can be a major obstacle on your path to financial freedom, but remember – you have the power to change your financial situation!

By implementing these strategies, you can take control of your debt, increase your net worth, and reach your financial goals. Start small, be consistent, and celebrate your progress along the way.

Take inspiration from the many individuals who have successfully navigated their way out of debt and built a solid financial foundation. Every step you take towards financial freedom is a victory!

Subscribe to new post

The One Liner

Useful Links

Order Related Queries

Useful Links

Order Related Queries

Trusted By |

@ 2020 The One Liner . All Rights reserved

The One Liner

Useful Links

Order Related Queries

Useful Links

Order Related Queries

Trusted By |